Property & Casualty Insights

Want Significant Savings and Greater Control Over Insurance Costs? Look at Loss Sensitive Options

AUGUST 2, 2022

Although the insurance market for primary casualty lines is stabilizing, organizations with below-average risk profiles or exposures to loss in certain states or industries continue to face upward rate pressure, especially those with a guaranteed cost program. In today’s challenging economic climate, insureds may find it increasingly difficult to maintain an affordable guaranteed cost program. Organizations should look at loss sensitive options to reduce their total cost of risk (TCOR).

Compared to guaranteed cost, loss sensitive programs offer companies more flexibility, and in some cases, significant cost savings.

Loss sensitive programs assume a larger portion of risk, typically through higher deductibles, which usually means lower premium. In USI Insurance Services’ experience, clients often see a 20% to 70% premium credit compared to guaranteed cost, depending on the deductible or retention level chosen. Higher risk retention will generally result in greater savings on premium.

Additionally, organizations with a good loss experience, effective loss control, and proactive claims management can reduce total cost of risk, reflected in lower premium and claims costs, among other benefits.

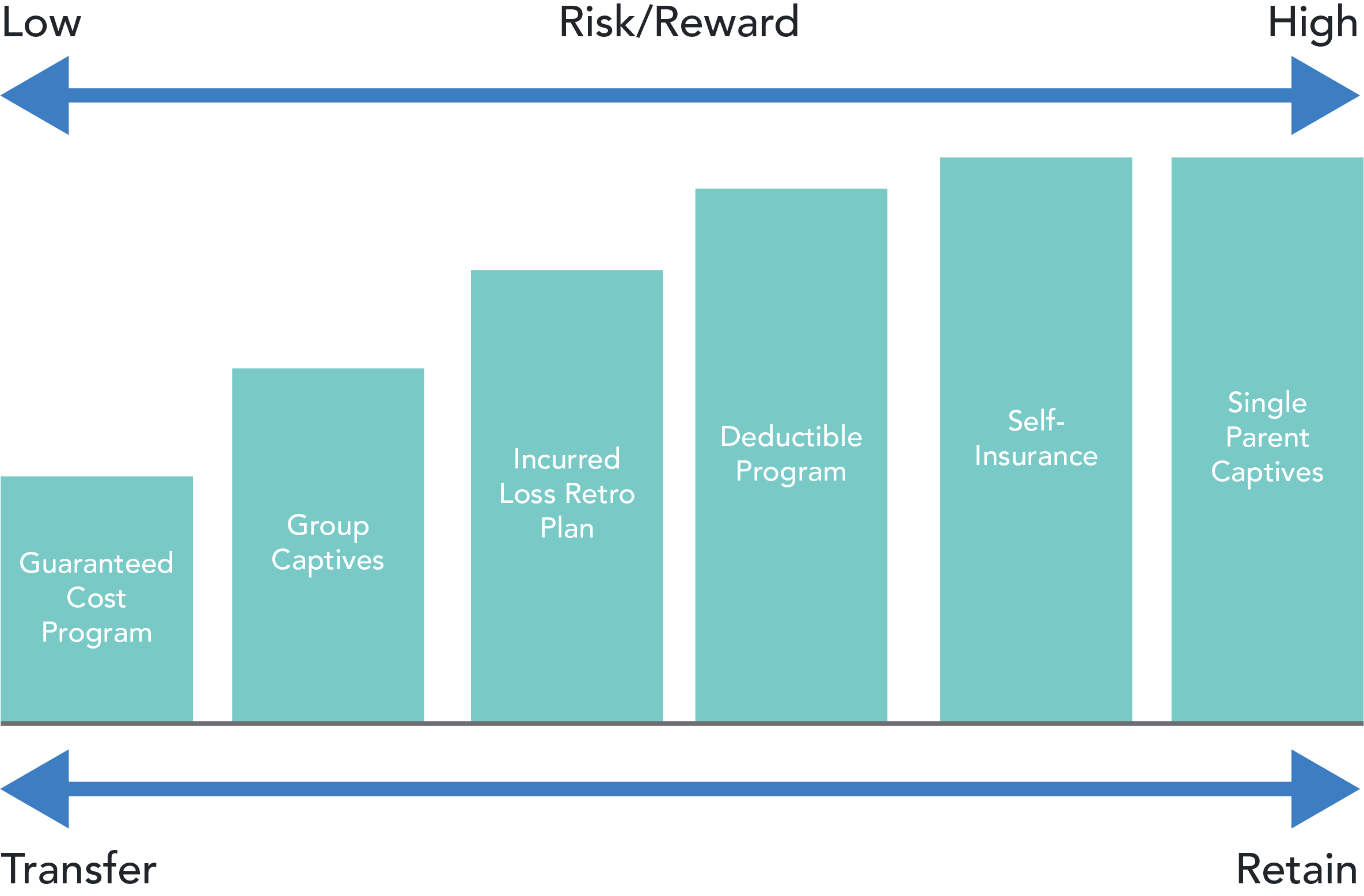

Comparing Loss Sensitive Programs

When considering a loss sensitive risk financing structure, there are several approaches:

Deductible Programs

These are similar to guaranteed cost — in most cases, the insurer performs all typical functions and handles claims. Insureds may have more opportunity to reduce costs if the insurer allows these services to be “unbundled” to third-party administrators (TPAs).

Benefits: Fixed premium is substantially less because the insured assumes a portion of the loss before any risk transfer to the insurer. In addition, the direct impact of losses to the bottom line is easy to see and address.

Considerations: The final cost of a large deductible plan can vary widely, depending on losses and any aggregate stop-loss coverage purchased. Insurers also often require collateral, usually in the form of a letter of credit (LOC), which can negatively impact an insured’s ability to borrow from its lines of credit. The cost for a bank to issue an LOC can also be expensive.

Dividend Plans

These provide insureds with the potential for a return of premium after the policy’s expiration. Sliding scale is the most common dividend plan type, wherein the dividend becomes payable based on a ratio of incurred losses to premium.

Benefits: Dividend plans are an attractive option because they offer a potentially lower premium if losses are low, and some dividend programs have no additional premium penalty if losses are high.

Considerations: In many sliding scale dividend plans, an insured may not earn dividends if the loss ratio is too high (often 65% or higher). The exact point at which dividends disappear varies from plan to plan, and from one premium size to another. Also, dividends are not guaranteed by an insurer year-over-year.

Incurred Loss Retrospective and Group Captives

Here, the insured prefunds any expected losses up to a certain level (subject to a maximum and minimum) and pays a fixed cost, including insurer profit and administration, excess charges, claims handling, loss control fees and premium taxes. The ultimate cost depends upon actual incurred losses, limited to the per-occurrence loss limitation. Group captives are similar to incurred loss retrospectives in that expected losses and fixed costs are prefunded.

Benefits: Group captives often have lower fixed costs and offer a more competitive maximum premium than incurred loss retrospective plans. By contrast, incurred loss retro may have more liberal collateral requirements since the insured is prefunding losses. Group captives are becoming increasingly attractive, especially for middle-market companies with premiums from $150,000 to more than $2 million.

Considerations: Losses that are prefunded in a group captive earn a more aggressive investment income return relative to an incurred loss retro; however, in a group captive, there is a requirement to share loss directly among the other group captive members.

Single Parent Captive Reinsurance

This represents the most strategic and formalized form of risk financing. Unlike a group captive, single parent captives usually insure the risk of a single company and its subsidiaries. Moreover, single parent captives typically work in concert with, not in replacement of, an existing deductible program.

Benefits: The goal is to help the “parent” achieve additional benefits above and beyond what its current deductible or self-insurance program can achieve. These can include tax benefits, the building of surplus in a dedicated insurance subsidiary, and the ability to access reinsurance markets, among others.

Considerations: Single parent captives are extremely complex and may not be a good fit for many insureds. For the economics of risk financing to work in this arrangement, the insured would need at least $2 million in retained losses.

Self-Insurance

Here, funds are set aside to cover losses that would ordinarily be covered by an insurance policy.

Benefits: Self-insurance can be cost-effective from a pricing perspective, depending on the industry and states in which the insured has payroll and operations, as certain markets can offer very competitive pricing.

Considerations: Since workers’ compensation is subject to statutory oversight, becoming an authorized self-insurer for this line of coverage requires initial and ongoing regulatory approval on a state-by-state basis, which can be a time-consuming administrative burden. There is also the misconception that there is no need to purchase any insurance; however, most states require excess insurance, based on the financial strength and size of the self-insured. In addition, the collateral requirements imposed by regulatory bodies can sometimes be inflexible.

How USI Can Help

When evaluating the different financing options available, USI helps clients determine the best structure through a detailed analysis of their risk management profile, risk philosophy and financial position. This meticulous process includes:

- Conducting loss forecasts and variability studies, as well as risk retention analysis

- Calculating compounded savings expected in varying loss scenarios

- Evaluating existing loss control and safety initiatives, and post-loss processes

- Assessing insurance companies, TPAs and loss control specialists

For companies seeking to reduce their TCOR, loss sensitive programs can be a great alternative to guaranteed cost structures.

To learn more about the various risk financing options for your organization, contact your USI representative or email pcinquiries@usi.com.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.