Retirement Consulting Insights

Fast-Forward to a Financially Secure Workforce

JUNE 7, 2022

Two years of economic uncertainty caused by the COVID-19 pandemic have been followed by inflation and rising prices for products and services. As a result, many people are struggling to save for retirement when faced with the more pressing priorities of paying for basic living expenses.

If your organization isn’t concerned, it should be. When employees struggle financially or don’t plan for the future, it can negatively impact your organization’s bottom line. Research shows that workers who are financially stressed are not fully focused on their duties and are more apt to have higher healthcare claims, absenteeism, reduced productivity and delayed retirement.

Employees who fail to retire at the expected age may remain on your payroll for several more years. Research conducted by Prudential in 2019 shows that for each year an employee delays retirement, the cost to an employer can be more than $50,000 per employee due to increased healthcare costs, lower productivity and higher salaries. For a company with 500 employees, the estimated cost is $2.25 million if only 15 workers delay retirement for three years.

Economic Struggles Impact Retirement Readiness

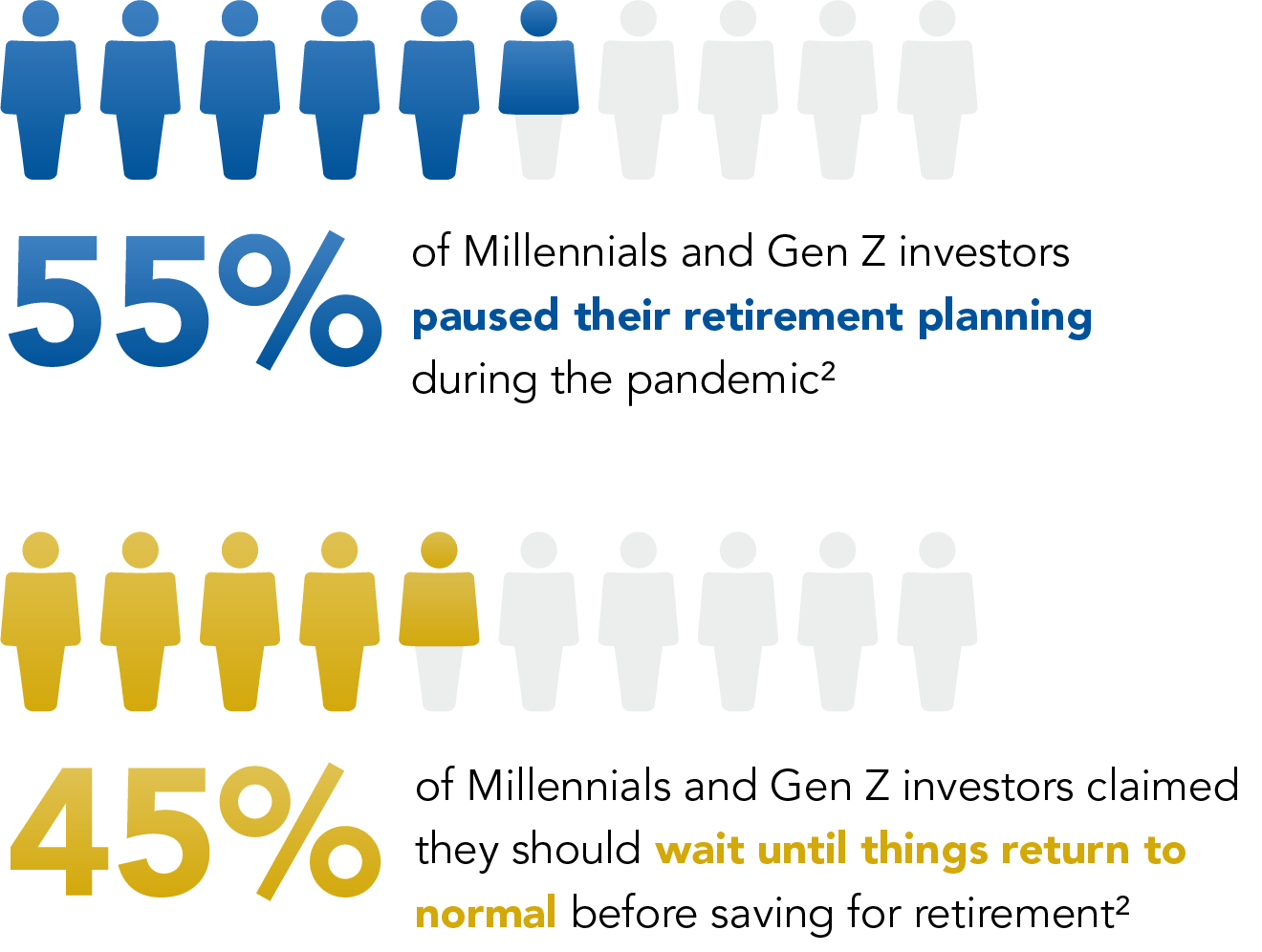

For workers who are 18 to 35 years old, postponing participation in a 401(k) or 403(b) savings plan may be a knee-jerk reaction to meeting the demands of monthly housing payments, student loans, transportation costs or daily living expenses. While younger workers may understand the need to save long-term, they may prioritize other immediate needs such as achieving short-term savings for emergencies.

Millennials and Gen Xers are the most insecure about their ability to cover monthly housing costs (rents/mortgages), so setting aside money for retirement is challenging for them.1 The youngest workers (Gen Z) are also hesitating to save for the future.

Employees who are closer to retirement also worry about rising prices, wondering if they’ve saved enough and if they’ll have to retire later than planned. Of Gen Xers who say the pandemic has negatively affected their retirement plans, nearly 30% state they are completely off track or will need four to five years to rebound.2

Unfortunately, these situations impact organizations of all sizes and in all industries. A 2020 survey by the Society for Human Resource Management revealed that 80% of employers said financial stress reduced employee performance — costing nearly $500 billion annually. In addition, the long-term effect of financial insecurity and retirement readiness can be extremely costly to employers.

Advantages of a Custom-Fit Recordkeeper

All employees in your workforce need to improve their financial security and become retirement ready. Your plan’s recordkeeper is key to helping your employees improve their financial security. Identifying an appropriate record keeper can be achieved with a retirement plan consultant dedicated to proactively meeting your plan’s needs.

The experts at USI Consulting Group (USICG) routinely conduct recordkeeper provider searches, aiming to match clients to an ideal recordkeeping solution to enhance the wellbeing of plan participants.

Case Study: Proactive Recordkeeper Improves Plan Participation and Contributions

A client recently engaged USICG to conduct a request for proposal (RFP) to change its 401(k) plan recordkeeper. The primary goal was to find a reputable recordkeeper that could meet the client’s needs with regards to employee education support, with priority on obtaining enhanced technology for employees’ retirement and financial wellness needs.

Through USICG’s customized RFP process and resources, we identified the right recordkeeper for the client’s plan and employees. By coupling the recordkeeper’s strong financial wellness tools and resources with USICG’s experienced team, the client implemented several plan design changes that enhanced the well-being of its plan’s participants. Plan participation increased to 98.5% from 61%, and the average deferral rate increased to 8.45% from 4.8%.

Consider your current recordkeeper’s services. Do they no longer meet the current plan structure? Do they fail to maximize current and future fee reduction opportunities — which may be negatively impacting your plan participants’ returns? Do they meet the need to educate and engage your employees to be more financially secure?

Helping Employees Obtain Security

Organizations have an opportunity to help employees acquire skills to improve income security and achieve the financial freedom to retire. The cost for an employer to not provide this guidance is too high. Our recent article, Employees Need Your Help to Achieve Retirement Readiness, highlights strategies to better prepare your employees for retirement and help offset the financial impact of delayed retirement to your organization.

A Trusted Partner for Your Recordkeeper Search

USICG has been helping employers enable their workforces to successfully plan and invest for retirement for over 45 years. Our specialized team evaluates the various recordkeeper options available to analytically determine the best customized fit for your organization’s retirement plan, and implements the best financial wellness program to improve participation and increase deferral rates.

To learn more about USICG’s solutions and how we can help you improve your employees’ financial security and retirement readiness, contact your local USICG representative, visit our Contact Us page, or reach out to us directly at information@usicg.com.

1 Morning Consult’s U.S. Consumer Spending Report (April 2022)

2 Fidelity Investments’ 2022 State of Retirement Planning Study

This information is provided solely for educational purposes and is not to be construed as investment, legal or tax advice. Prior to acting on this information, we recommend that you seek independent advice specific to your situation from a qualified investment/legal/tax professional.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.